Sustainability has emerged as a key strategic priority in the GCC region. From the UAE to Saudi Arabia, the shift toward low-carbon economies, green technologies, and climate-resilient policies is driving transformation across industries.

For public sector organizations, sustainability is mostly focused on achieving policy goals, fostering societal well-being, and addressing global challenges such as climate change and resource scarcity. For private sector entities meanwhile, sustainability is often a driver of corporate social responsibility, brand reputation, market competitiveness, and innovation.

Yet navigating the sustainability transition is easier said than done. The development and implementation of plans can be a challenge, due to a range of factors including stakeholder priorities, financial constraints, and operational environments.

Samer Taleb, Director of Strategy Consulting at Knowledge Group Consulting, walks through the main challenges that come with sustainability, and outlines a framework for how leaders can align their sustainability goals with measurable outcomes and successfully drive progress in their green journey.

Key Indicators of Sustainability

The shift to sustainability is accelerating at the global and regional level. An overview of five indicators:

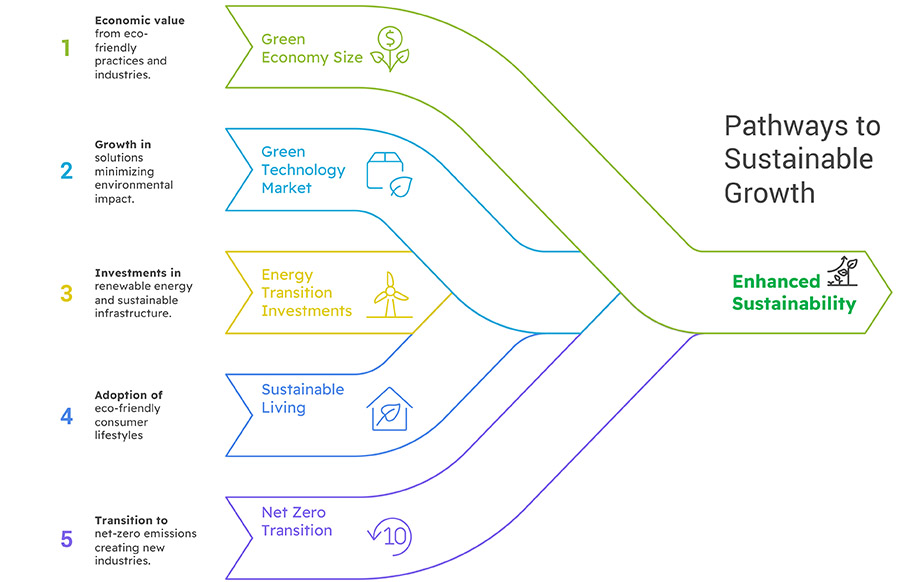

Green Economy Size

According to The United Nations Environment Programme (UNEP), the global green economy is now valued at $7.2 trillion, positioning it as the second-best-performing industry globally over the past decade. This demonstrates the significant economic potential of sustainable practices and investments.

Green Technology Market

The global green technology market is projected to grow from $17 billion in 2023 to over $105 billion by 2032, reflecting a compound annual growth rate (CAGR) of 22.4% from 2024 to 2032, according to the World Economic Forum. This growth is driven by increasing demand for innovative solutions to environmental challenges.

Energy Transition Investments

Global investments in clean energy technologies exceeded $1.7 trillion in 2023, marking a 17% increase from the previous year, as part of the global transition to sustainable energy sources, according to the World Bank. This highlights the increasing financial commitment to transitioning away from fossil fuels.

Sustainable Living

According to the United Nations Environment Programme (UNEP), 71% of global consumers are making changes to their lifestyles and purchasing decisions to live more sustainably, indicating the rising importance of environmental impact in consumer choices. This shift in consumer behavior is driving demand for sustainable products and services.

Net Zero Transition

Transitioning to a net-zero emissions environment by 2050 could create new industries worth $10.3 trillion to the global economy, according to Oxford Economics. This underscores the economic opportunities associated with addressing climate change and reducing carbon emissions.

Achieving net-zero emissions requires significant investments in renewable energy, energy efficiency, and carbon capture technologies. These investments will not only reduce environmental impact but also stimulate economic growth and create new job opportunities.

Businesses and governments that embrace the net-zero transition can position themselves as leaders in the green economy and attract investors, customers, and talent who prioritize sustainability.

The Challenges that come with Sustainability

At an organizational level, the challenges associated with developing and implementing sustainability strategies can be grouped into structural challenges, operational challenges, and financial challenges. These categories include several sub-challenges that are critical to address for success.

Structural Challenges

Regulatory complexity and leadership/governance gaps hinder strategic alignment.

Regulatory Complexity

Organizations often face a web of conflicting or ambiguous regulations. Public sector entities might encounter discrepancies between local and national policies, while private firms must navigate diverse global standards. This complexity increases compliance costs and operational uncertainty.

Leadership and Governance

Gaps Effective sustainability initiatives require strong governance frameworks. Without this, both public and private organizations risk fragmented efforts and a lack of strategic direction. Clear accountability and well-defined roles are essential for driving meaningful progress.

Operational Challenges

Technological barriers and stakeholder resistance impede practical implementation.

Technological Barriers

The lack of access to or adoption of innovative technologies hinders progress. Legacy systems in manufacturing may prevent efficient resource use and emissions reductions. Bridging this technological gap is crucial for achieving sustainability goals.

Stakeholder Resistance

Resistance from employees, communities, or partners can derail projects. Miscommunication or insufficient engagement often causes mistrust or lack of support for sustainability initiatives. Engaging stakeholders through transparent communication and collaboration is key.

Financial Challenges

Budget constraints and economic volatility disrupt long-term sustainability plans.

Budget Constraints

Public sector entities may deprioritize sustainability initiatives in favor of pressing short-term needs, while businesses might find it challenging to justify the high initial costs of green investments. Creative financing solutions and long-term cost-benefit analyses are essential.

Economic Volatility

Market fluctuations and economic downturns can disrupt sustainability plans, forcing organizations to delay or abandon initiatives. Building resilience into sustainability strategies and diversifying funding sources can help mitigate this risk.

From Assessment to Implementation

Effective sustainability strategies involve several critical factors, spanning from the assessment of the current state to the implementation and monitoring of initiatives. These factors must be addressed comprehensively to ensure success.